Mynt, Inc. filed its draft preliminary prospectus on June 27, 2026, and the filing indeed confirms that the GCash IPO is headed for the Philippine Stock Exchange. It puts the company’s financials on the record. For the first time, Filipino investors can read the actual numbers behind the country’s most popular and widely used finance app: revenue, profit, loan portfolio, and the risks the company itself believes could hurt the business.

I have read through the prospectus in detail, and this analysis covers what I consider the most important parts: how the offer is structured, what the financials show, where the money is coming from and going to, and the risk factors that deserve extra scrutiny. This is not investment advice. This is a deep dive analysis of a public document, written to help you understand what you would be buying when the IPO goes live later this year.

One thing to keep in mind is that this is a draft preliminary prospectus. Several figures – most notably the exact peso allocation of the IPO proceeds – are still marked as placeholders in the document. Where that is the case, I say so rather than guess.

Table of Contents

The Offer at a Glance

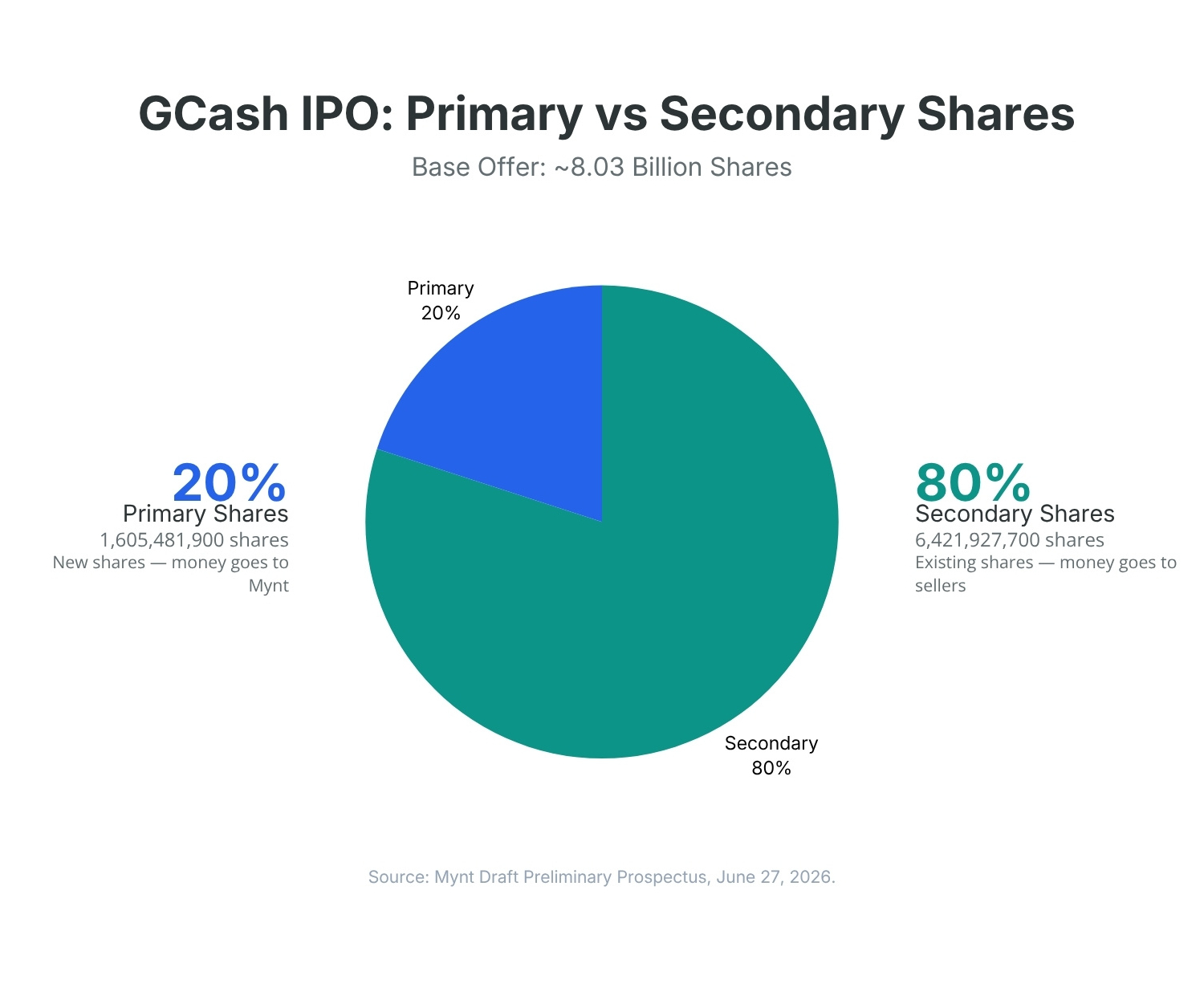

Mynt is offering up to 8,027,409,600 common shares at an indicative price of up to ₱10.00 per share. That base offer is worth as much as ₱80.3 billion. If the overallotment option of up to 1,204,111,400 additional shares is fully exercised, total proceeds reach approximately ₱92.3 billion, which would make it the largest IPO in Philippine history.

The shares will list on the PSE Main Board under the ticker “GCASH.” Here are some key details of the upcoming GCash IPO:

| Item | Detail |

|---|---|

| Ticker symbol | GCASH |

| Indicative offer price | Up to ₱10.00 per share |

| Primary shares (new) | 1,605,481,900 |

| Secondary shares (existing) | 6,421,927,700 |

| Overallotment option | Up to 1,204,111,400 |

| Base offer proceeds | Up to ₱80.3 billion |

| Maximum proceeds | ~₱92.3 billion |

| Public float | 12.0% (13.8% with overallotment) |

| Offer period | October 5–9, 2026 |

| Listing date | October 19, 2026 |

The Secondary-Sale Question

The most important structural feature of this IPO is hidden in the share split. Of the 8.03 billion shares in the base offer, only about 1.6 billion are primary shares, which are newly issued stock whose proceeds go to Mynt itself. The remaining 6.4 billion, roughly 80% of the offer, are secondary shares sold by existing shareholders.

This is important because it changes what the IPO is for. When a company raises money mostly through primary shares, the cash funds its expansion – new products, new markets, and more lending capital. When most of the offer is secondary, the cash largely goes to early backers cashing out part of their stake. The selling shareholders named in the prospectus include Ant International, ASP Philippines LP, and several other institutional investors.

A large secondary component is not inherently a red flag. Early investors in a 14-year-old company have every reason to seek partial liquidity, and the presence of sophisticated buyers doesn’t mean the price is wrong. However, it means that prospective investors should read the valuation on its own merits rather than assuming the bulk of their money is funding future growth. The dilution table in the prospectus confirms the structure: after the offer, existing shareholders retain 86.2% of the company and new investors hold 13.8%, assuming that the overallotment is fully exercised.

Financial Performance

The numbers describe a company that is both large and still growing fast.

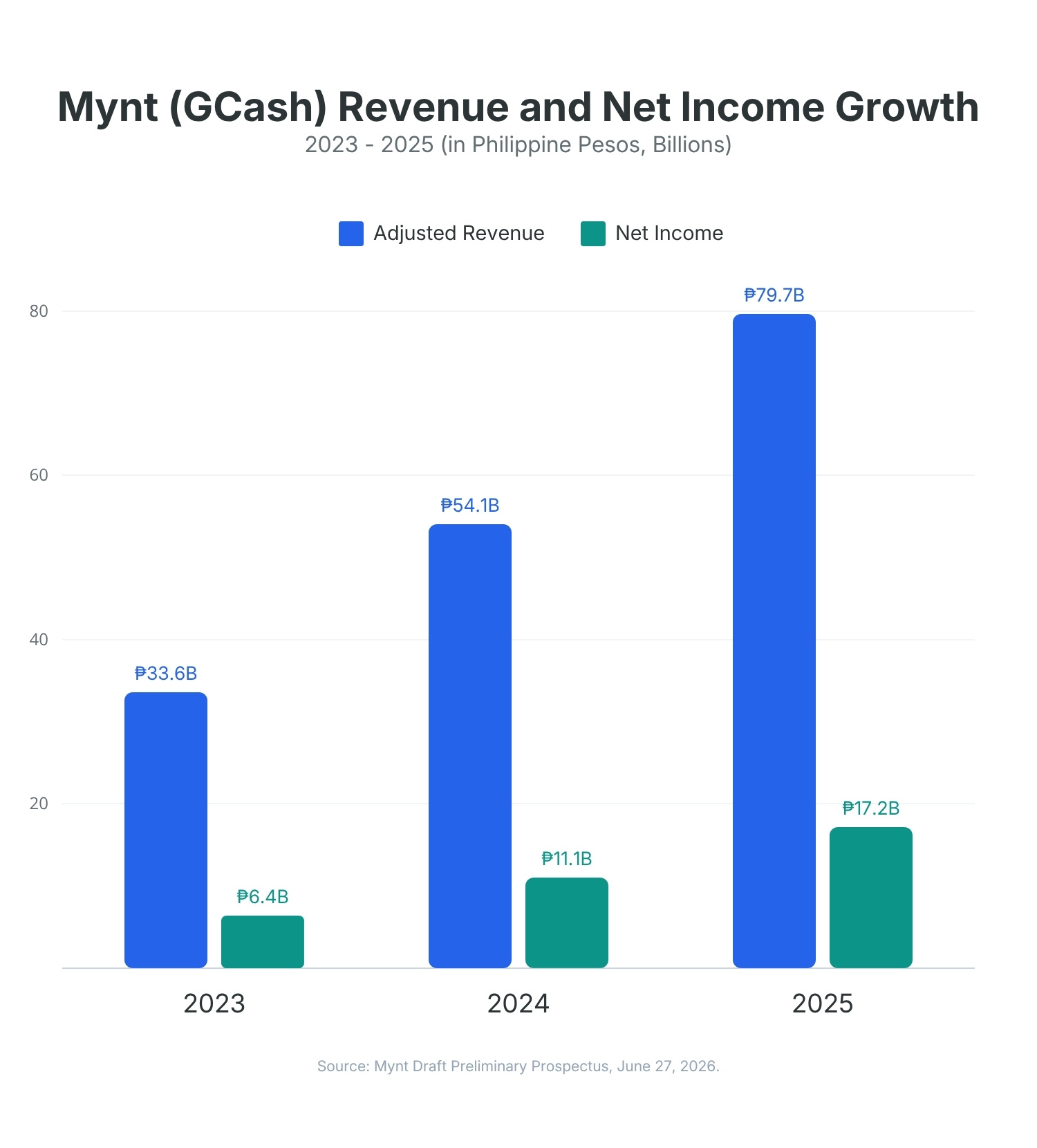

Adjusted revenues rose from ₱33.6 billion in 2023 to ₱54.1 billion in 2024 to ₱79.7 billion in 2025. Net income over the same period climbed from ₱6.4 billion to ₱11.1 billion to ₱17.2 billion. The first quarter of 2026 brought ₱20.7 billion in revenue and ₱5.6 billion in net income, both up from the same quarter a year earlier (₱18.1 billion and ₱4.5 billion).

| Metric | 2023 | 2024 | 2025 | Q1 2026 |

|---|---|---|---|---|

| Adjusted revenue | ₱33.6B | ₱54.1B | ₱79.7B | ₱20.7B |

| Net income | ₱6.4B | ₱11.1B | ₱17.2B | ₱5.6B |

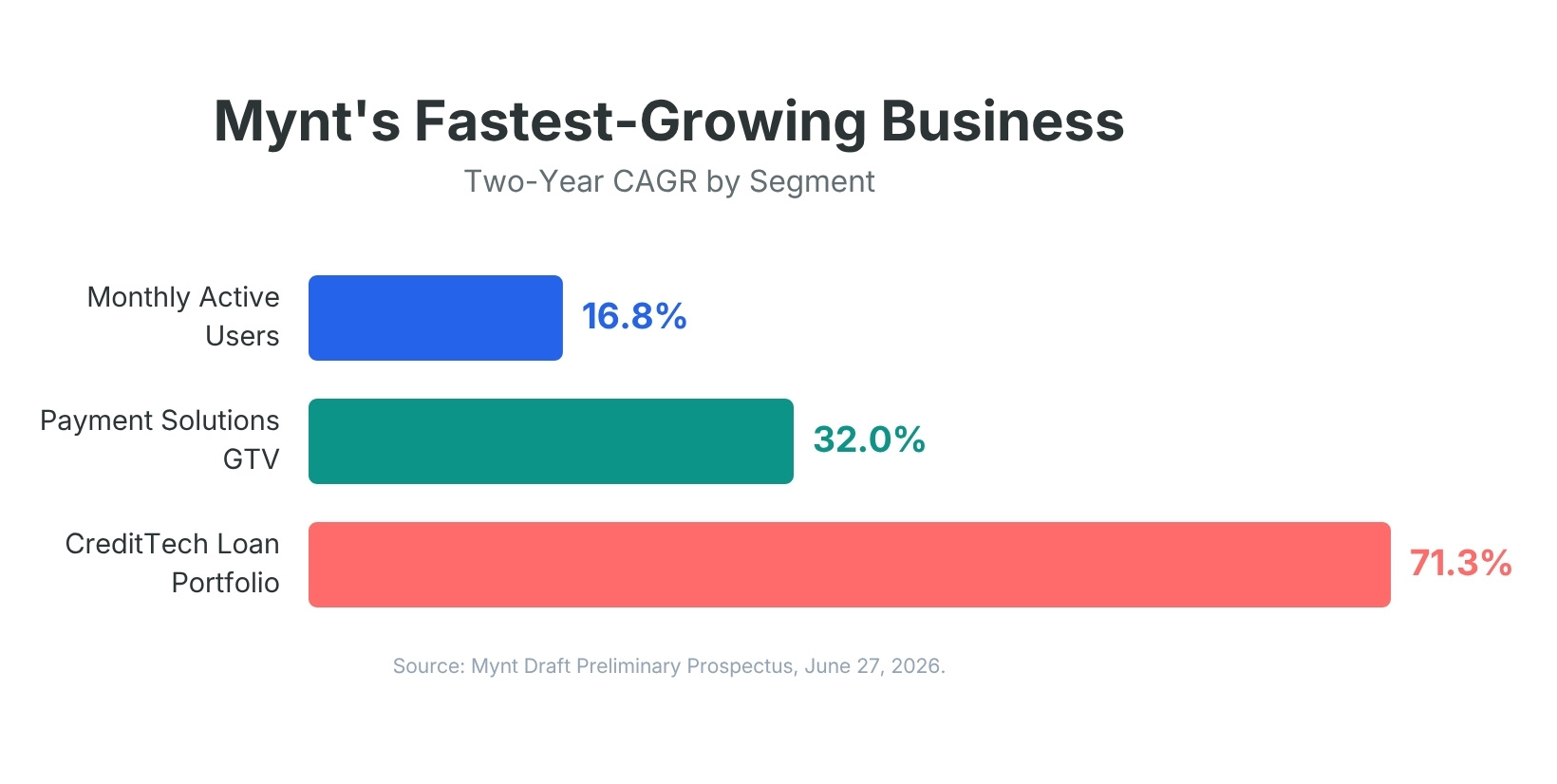

Mynt reports a two-year compound annual growth rate (CAGR) of 16.8% in monthly active users, 32.0% in Payment Solutions gross transaction value, and 71.3% in its total loan portfolio. That last figure is the one I would watch more closely. The CreditTech (lending) business is growing far faster than payments, and the total loan portfolio reached ₱64.07 billion as of March 31, 2026. Lending is more profitable than payment processing, but it also carries credit risk that pure payment volume doesn’t.

The Numbers Behind “GCash is a Verb”

The prospectus reveals how embedded GCash has become in the Filipino way of life. As of March 31, 2026, the app reported 40.4 million monthly active users. Citing Frost & Sullivan, the filing places that at 55% of the Philippines’ total adult population and four times the monthly active users of its closest competitor.

The supporting infrastructure numbers are equally telling: 1.3 million cash-in and cash-out touchpoints, 2.1 million QR Ph merchants, and more than 3,000 biller and government partners. For the first quarter of 2026 alone, Payment Solutions gross transaction value reached ₱4,748.4 billion. These figures explain why the company can describe itself as national infrastructure rather than simply an app, and why the regulatory risks below carry real weight.

Online Gaming Risk

Mynt states plainly that a portion of its Payment Solutions revenue across every reporting period came from transactions connected to licensed online gaming, processed mainly through the GLife platform inside the GCash app.

This exposes the company to a regulatory environment that the prospectus describes as dynamic and uncertain. The filing notes that several legislative bills have been filed in Congress proposing measures that range from barring e-wallets from processing online gaming transactions to banning gaming advertising inside super app ecosystems. It also cites a BSP memorandum issued on August 14, 2025, which required supervised institutions to remove in-app gambling access from their mobile platforms.

The prospectus doesn’t say what share of revenue comes from online gaming, so the exposure is hard to size. What’s clear is the direction regulators are heading, and if lawmakers tighten the rules, a revenue stream the company relies on could be affected. For a prospective investor, this is the kind of risk that doesn’t show up in a revenue chart, but one worth weighing seriously before investing.

Use of Proceeds: Still Incomplete

The prospectus lists four intended uses for the net proceeds of the primary offer: CreditTech growth, product development, strategic cash reserves, and general corporate purposes. However, the actual peso amounts and percentages for each are left as placeholders, to be filled in before the filing is finalized.

The CreditTech allocation is described as funding the expected growth of the lending book over the coming years. Product development is tied to scaling business and cross-border offerings, including services for overseas Filipinos, and to investment in the company’s data and AI systems. The strategic cash reserve is explicitly linked to possible future acquisitions, with the 2025 purchase of ECPay cited as the template. Until the final figures appear, though, investors cannot yet see how much of their money is going toward growth versus how much is being held in reserve.

No Promises of Dividends Yet

Investors hoping for a predictable payout should read this section carefully. Mynt states that it doesn’t have a fixed dividend policy. Any future dividends will depend on earnings, cash flow, financial condition, and other factors, and will be declared at the board’s discretion out of unrestricted retained earnings.

This is a common position for a high-growth company that would rather reinvest profit than commit to a payout ratio, and it’s consistent with the lending-led expansion that the financials show. It does mean, however, that for the near term this is a stock to hold for capital appreciation rather than income.

Who’s Underwriting It

The syndicate signals the scale and international ambition of the deal. Morgan Stanley & Co. International, J.P. Morgan Securities, and UBS AG Singapore Branch are the joint global coordinators and bookrunners. Jefferies Singapore Limited is the international joint bookrunner.

On the domestic side, BPI Capital Corporation and BDO Capital & Investment Corporation are the lead underwriters. The presence of three global banks of that tier reflects an offer being marketed to international institutional investors, not only the local market.

Frequently Asked Questions

What is the ticker symbol for the GCash IPO?

Mynt’s shares are expected to trade on the Philippine Stock Exchange Main Board under the ticker symbol “GCASH,” according to the draft preliminary prospectus filed on June 27, 2026. The listing remains subject to SEC and PSE approval.

How much is the GCash IPO raising?

The base offer of up to 8,027,409,600 shares at up to ₱10.00 each could raise as much as ₱80.3 billion. With the overallotment option fully exercised, total proceeds could reach approximately ₱92.3 billion, which would be the largest IPO in Philippine history.

When can I buy GCash shares?

The offer period is scheduled to run from October 5 to October 9, 2026, with the listing and settlement date targeted for October 19, 2026. These dates are stated in the draft prospectus and remain subject to regulatory approval and market conditions, so they may change.

Is most of the IPO new shares or existing shares?

Most of the base offer is existing shares. Of the 8.03 billion shares offered, about 1.6 billion are new (primary) shares that raise money for Mynt, while roughly 6.4 billion are existing (secondary) shares sold by current shareholders. After the offer, existing shareholders retain 86.2% of the company.

Will GCash pay dividends?

The prospectus states that Mynt does not have a fixed dividend policy. Future dividends will depend on earnings, cash flow, and financial condition, and will be declared at the board’s discretion. There is no committed payout ratio at this stage.

In a Nutshell

The Mynt prospectus describes a profitable, fast-growing company at the heart of Philippine digital finance, and the headline numbers – ₱79.7 billion in 2025 revenue, ₱17.2 billion in net income, 40.4 million monthly users – are genuinely strong.

The questions worth asking are the structural ones: the heavy secondary-sale component, the fast-growing but credit-exposed lending book, the unresolved use-of-proceeds figures, and the online gaming regulatory overhang.

This analysis was written on June 29, 2026, based on the draft preliminary prospectus dated June 27, 2026. Because several figures in that document are still placeholders, I expect to revisit this once the final prospectus and offer price are confirmed.

As always, nothing here is investment advice. Do your own due diligence and consult a licensed financial adviser before deciding.