Do you want to earn passive income with hardly any effort? Then the Pag-IBIG MP2 savings program might be for you. It’s a voluntary savings program for members of the Pag-IBIG Fund where you can earn tax-free income at higher dividends than other low-risk investment schemes.

If you’re interested about how to invest and earn money from Pag-IBIG MP2, then continue reading. We’ve come up with this comprehensive guide on the Modified Pag-IBIG II savings program which will help you get started with Pag-IBIG MP2.

Disclaimer: This article is for informational purposes only and should not be considered as financial investment advice.

What is Pag-IBIG MP2?

You might have read the recent news about the staggering 7.23% dividend rate of Pag-IBIG MP2 for the year 2019, which piqued the interest of many would-be investors. So what is Pag-IBIG MP2 and how does one earn money from it?

The Modified Pag-IBIG II Savings Program or Pag-IBIG MP2 is a voluntary savings program by the Home Development Mutual Fund (HDMF) or commonly known as the Pag-IBIG Fund. It is open to all Pag-IBIG Fund members as well as former members and pensioners.

Compared to the regular savings program which is mandatory to all Pag-IBIG members, the Pag-IBIG MP2 savings program has a higher dividend rate. Over the last 5 years, the average dividend rate for Pag-IBIG MP2 is 7.10% while the average dividend rate for Pag-IBIG regular savings is 6.60%.

Pag-IBIG MP2 has a maturity period of 5 years, compared to 20 years for Pag-IBIG regular savings. You can choose to receive your dividends annually or after the maturity period. You can even withdraw your savings anytime you want before the maturity date, with the caveat that you will not receive the full dividends.

Unlike the stock market and other forms of investment, you don’t need to study financial investing or perform technical analysis. You just sit back and relax while you watch your money grow. Pag-IBIG Fund dividends are tax free so you don’t have to worry about withholding taxes eating into your profits.

The Pag-IBIG Fund invests your money in various assets and investments such as corporate bonds, government securities, time deposits, short-terms loans and housing loans. As required by law, 70% of Pag-IBIG MP2 funds are invested in housing loan programs.

The Pag-IBIG MP2 savings program is fully guaranteed by the Philippine government, which makes it one of the safest forms of investments available. Obviously, there are inherent risks with any kind of investment, but since Pag-IBIG MP2 is guaranteed by the government, you will still get your money back in the unlikely event that the fund loses money.

The beauty of Pag-IBIG MP2 is that it gives you flexibility in your savings. Unlike other investment vehicles like variable universal life insurance (VULs) wherein you have to pay a fixed amount for the lifetime of the contract, you can save any amount of money in your Pag-IBIG MP2 account. For example, you can save ₱1,000 for this month, ₱2,000 the next month and then ₱500 for the succeeding month. You are not restricted as to how much you can save for the month. You can even skip months if you don’t have the money to save.

The Pros and Cons of Pag-IBIG MP2

Before you shell out your hard-earned money, it’s time to know what benefits you can accrue from Pag-IBIG MP2. Is it the right investment vehicle for you? Knowing the advantages and disadvantages of Pag-IBIG MP2 will help you determine if it’s the perfect investment program to grow your money.

Advantages of Pag-IBIG MP2

- It has a low barrier to entry. Anyone can join as long as he or she is a Pag-IBIG member.

- It’s easy to open an account through the Internet. You only need to submit an application form and a bank account.

- Risks are minimal because the fund is guaranteed by the Philippine government. If the fund loses money, you’ll still get your investment back.

- You can save as low as ₱500, making it perfect for small-time investors.

- There’s no limit to how much you can invest. You can put up millions if you want to.

- You can open two or more Pag-IBIG MP2 accounts.

- You don’t have to study investing; the Pag-IBIG Fund does everything for you.

- You earn passive income. You don’t have to do any work except to save money.

- Your earnings and dividends are tax-free and there are no hidden fees.

- Dividends are higher compared to regular Pag-IBIG savings, bank savings and time deposits.

- It’s voluntary savings so you can save anytime you want. You can save on a monthly, annual or one-time basis.

- It’s flexible so you can skip your monthly contributions without penalty.

- You can withdraw your money anytime for whatever reason. However, you will lose half or all of your dividends unless your reason is valid and approved by the Pag-IBIG Fund.

- Several payment options are available at Pag-IBIG offices, accredited collecting partners, or online payment facilities.

- You can conveniently check your MP2 savings online in your Virtual Pag-IBIG account.

Disadvantages of Pag-IBIG MP2

- The maturity period is 5 years. If you withdraw your money before the maturity date, you will not receive the full dividends.

- After the maturity date, your money will earn the same dividends as Pag-IBIG regular savings. Two years after the maturity date, your money will earn nothing.

- You need to open a new Pag-IBIG MP2 account to continue earning after 5 years.

Who Are Qualified to Join Pag-IBIG MP2?

The following are qualified to enroll in the Pag-IBIG MP2 savings program:

- Active contributing members of the Pag-IBIG Fund.

- Former Pag-IBIG members with source of income.

- Pensioners with at least 24 monthly contributions prior to retirement.

How to Enroll in Pag-IBIG MP2

There are two ways to enroll in Pag-IBIG MP2:

- Online enrollment through the Pag-IBIG website.

- Submission of application form at the Pag-IBIG office.

We recommend enrolling through the Pag-IBIG website because it’s more convenient. You can just use any computer or mobile device with an Internet connection. After enrolling in the Pag-IBIG MP2 savings program, you will immediately be issued your unique Pag-IBIG MP2 account number.

If you prefer to enroll at the Pag-IBIG office, you may download the enrollment form here.

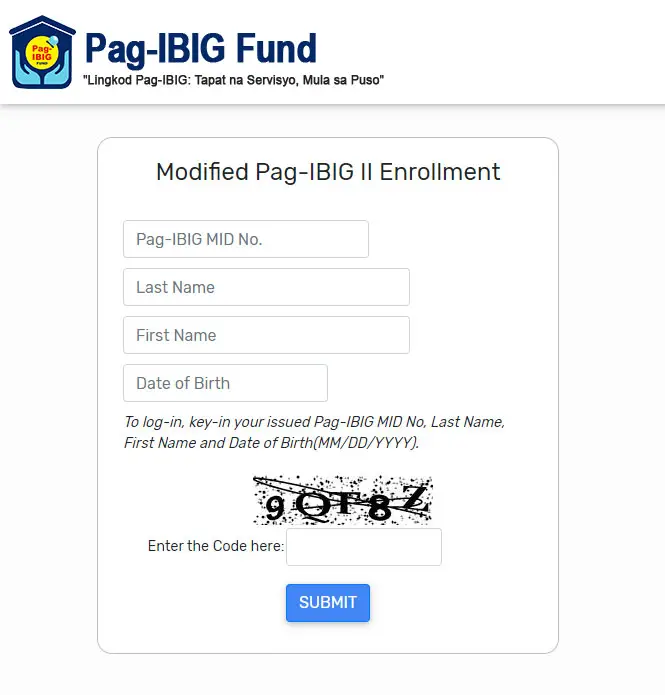

Pag-IBIG MP2 Online Enrollment Process

Go to the Pag-IBIG MP2 online enrollment website here.

Fill out your Pag-IBIG membership ID or MID number, last name, first name, and date of birth in MM/DD/YYYY format. Enter the captcha code and click the SUBMIT button.

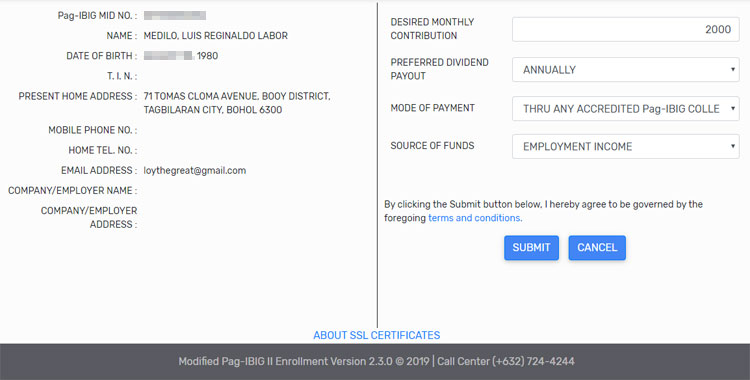

Review your enrollment details. Enter or choose the following required information:

- Desired monthly contribution (minimum of ₱500)

- Preferred dividend payout:

- Annually

- 5-year term

- Mode of payment:

- Salary deduction

- Over-the-counter

- Through accredited Pag-IBIG collecting partners

- Source of funds:

- Employment income

- Savings/deposits

- Property sale

- Sale of share or other investment

- Loan

- Company sale

- Company profits/dividends

- Gift

- Maturity/surrender of life policy

- Other income sources

If everything is correct, click the SUBMIT button.

You’re now enrolled in Pag-IBIG MP2 savings program. Save or copy your Pag-IBIG MP2 account number for your reference.

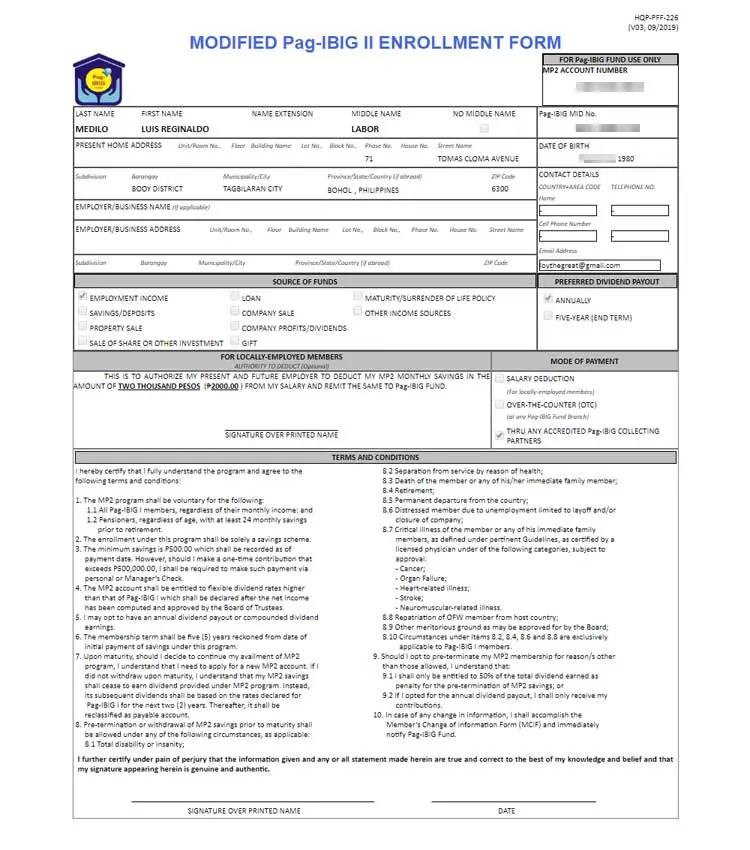

Print the filled-out enrollment form, sign it, and submit it to the nearest Pag-IBIG Fund branch. Provide a valid ID and the ATM card or passbook of your nominated bank account (this is where your dividends will be deposited).

Afterward, you can start paying your MP2 contributions at the Pag-IBIG office or any accredited collecting partner.

How to Pay Your Pag-IBIG MP2 Contributions

You can remit your savings to the Pag-IBIG office nearest you or through Pag-IBIG accredited collection partners such as Bayad Center, M Lhuillier, SM Business Center or ECPay. Members abroad may pay their contributions through collecting agents and overseas remittance partners like Philippine National Bank (PNB), Asia United Bank, CashPinas, I-Remit, and Ventaja.

It’s also possible to pay your Pag-IBIG MP2 savings contributions online. Read this article to learn how to pay your Pag-IBIG contributions online via GCash, PayMaya, Coins.ph and other online payment platforms.

After paying your contributions, you can check it online through the Virtual Pag-IBIG website. Click here to learn how to check your Pag-IBIG contributions online.

Employed individuals may also opt to have their MP2 savings deducted from their salaries. To do so, the member must indicate the business name and address of his or her employer in the application form.

How Much Should You Invest?

There’s no limit as to how much you want to invest in Pag-IBIG MP2. You can invest as low as ₱500 (which is the minimum) or as much as ₱1 million (or even more).

A personal or manager’s check is required for amounts larger than ₱500,000, instead of cash.

Remember, the more you save, the more you may earn.

How Often Should You Save?

There are two schools of thought with regard to the frequency of your Pag-IBIG MP2 savings. Some people recommend investing monthly while others believe that saving annually is better.

According to Pesolab, saving annually gives you better gains compared to saving monthly. If you save ₱500 per month based on a 5-year average dividend rate of 7.10%, your total savings after 5 years will be ₱35,614. On the other hand, if you save ₱6,000 per year, your total savings after 5 years will be ₱36,479.

A one-time investment will also give higher dividends compared to investing regularly. A one-time lump sum investment of ₱30,000 will earn you a total savings of ₱41,277 after 5 years. This is significantly higher than what you’ll earn from either monthly and annual savings.

It’s up to you what “strategy” you want to follow. If you have a large amount of cash lying around, then it’s better to invest annually or one-time to earn higher dividends. But if not, you still can’t go wrong with regular monthly contributions. It’s certainly better than putting your money in the bank.

Once again, this article is for informational purposes only and shouldn’t be considered as financial advice. Seek the advice of a licensed investment professional before investing your hard-earned money.

When Will You Receive the Dividends?

You may choose to receive your dividends annually or after the end of the 5-year maturity period.

Annual dividends will be credited to your savings or checking account with a Pag-IBIG accredited bank such as Land Bank of the Philippines or the Development Bank of the Philippines. Those who have no bank accounts in the Philippines, such as OFWs, will receive their Pag-IBIG MP2 dividends via check.

Compounded dividends may be claimed anytime after the 5-year maturity period. Unclaimed MP2 savings will continue earning dividends for two more years based on the Pag-IBIG regular savings rates. After the end of the additional two-year period, your savings will no longer earn dividends and must be claimed as soon as possible.

You are free to reapply for a new Pag-IBIG MP2 savings account once your existing MP2 savings account reaches maturity. Remember that you can open and maintain multiple savings accounts.

Is It Possible to Withdraw Your Savings Before Maturity?

Yes, you may withdraw your Pag-IBIG MP2 savings anytime within the 5-year lock-in period. However, you will only receive your total savings plus half (50%) of the total dividends earned. Members who opted for annual payouts will only receive their total savings and no dividends.

Exceptions are total disability, insanity, death, health-related work separation, retirement, unemployment due to job layoffs or company closure, critical illness, permanent departure from the country, OFW repatriation, and other reasons approved by the Pag-IBIG Fund. Members who withdraw their savings due to the aforementioned reasons will receive their total savings and dividends up to the time of the withdrawal.

How Much Will You Earn From Pag-IBIG MP2?

Your earnings from Pag-IBIG MP2 will depend on the fund’s performance. Take a look at the tables below for a sample computation of your dividends based on the average rate of 7.10% over the past 5 years. Take note that past performance is not an indicator of future results.

Annual Dividends (₱1,000/Month Savings)

| Year | Accumulated Savings | Annual Dividends | Accumulated Total |

|---|---|---|---|

| 1 | 12,000.00 | 461.50 | 12,461.50 |

| 2 | 24,000.00 | 1,313.50 | 25,775.00 |

| 3 | 36,000.00 | 2,165.50 | 39,940.50 |

| 4 | 48,000.00 | 3,017.50 | 54,958.00 |

| 5 | 60,000.00 | 3,869.50 | 70,827.00 |

Compounded Dividends (₱1,000/Month Savings)

| Year | Accumulated Savings | Annual Dividends | Accumulated Total |

|---|---|---|---|

| 1 | 12,000.00 | 461.50 | 12,461.50 |

| 2 | 24,461.50 | 1,346.26 | 25,807.76 |

| 3 | 37,807.76 | 2,293.85 | 40,101.61 |

| 4 | 52,101.61 | 3,308.71 | 55,410.32 |

| 5 | 67,410.32 | 4,395.63 | 71,805.95 |

Annual Dividends (₱1 Million One-Time Savings)

| Year | Accumulated Savings | Annual Dividends | Accumulated Total |

|---|---|---|---|

| 1 | 1,000,000.00 | 71,000.00 | 1,071,000.00 |

| 2 | 0 | 71,000.00 | 1,142,000.00 |

| 3 | 0 | 71,000.00 | 1,213,000.00 |

| 4 | 0 | 71,000.00 | 1,284,000.00 |

| 5 | 0 | 71,000.00 | 1,355,000.00 |

Compounded Dividends (₱1 Million One-Time Savings)

| Year | Accumulated Savings | Annual Dividends | Accumulated Total |

|---|---|---|---|

| 1 | 1,000,000.00 | 71,000.00 | 1,071,000.00 |

| 2 | 0 | 76,041.00 | 1,147,041.00 |

| 3 | 0 | 81,439.91 | 1,228,480.91 |

| 4 | 0 | 87,222.14 | 1,315,703.05 |

| 5 | 0 | 93,414.91 | 1,409,117.96 |

How to Compute Pag-IBIG MP2 Dividends

Here’s how to calculate your dividends with Pag-IBIG MP2, so you’ll know how much your money will grow based on the dividend rate that will be announced by the Pag-IBIG Fund at the end of each year.

The formula for computing your Pag-IBIG MP2 dividends goes like this:

Cumulative Savings x Dividend Rate ÷ 12 = Monthly Dividend

Take note that the dividend rate in this formula must be in decimal form. For instance, 7.10% is 0.0710.

If you save ₱1,000 at a dividend rate of 7.10%, your monthly dividend is ₱5.92 (rounded off). The computation is: 1,000 multiplied by 0.0710 and divided by 12 equals 5.92.

Then if you save ₱1,000 the next month, your cumulative or accumulated savings is now ₱2,000 (1,000 + 1,000). Using the formula, your monthly dividend is 19.28. The computation is 2,000 x 0.0710 ÷ 12 = 11.83.

Check out the table below for a sample computation if you save ₱1,000 a month consistently at a dividend rate of 7.10%:

| Month | Monthly Savings | Accumulated Savings | Monthly Dividend |

|---|---|---|---|

| January | 1,000.00 | 1,000.00 | 5.92 |

| February | 1,000.00 | 2,000.00 | 11.83 |

| March | 1,000.00 | 3,000.00 | 17.75 |

| April | 1,000.00 | 4,000.00 | 23.67 |

| May | 1,000.00 | 5,000.00 | 29.58 |

| June | 1,000.00 | 6,000.00 | 35.50 |

| July | 1,000.00 | 7,000.00 | 41.42 |

| August | 1,000.00 | 8,000.00 | 47.33 |

| September | 1,000.00 | 9,000.00 | 53.25 |

| October | 1,000.00 | 10,000.00 | 59.17 |

| November | 1,000.00 | 11,000.00 | 65.08 |

| December | 1,000.00 | 12,000.00 | 71.00 |

| TOTAL | 12,000.00 | 12,000.00 | 461.50 |

If you chose the annual dividend payout option, your dividend will be released annually and only your accumulated savings will roll over to the succeeding year.

But if you chose the compounded dividend option, the annual dividend will be added to your accumulated or cumulative savings at the end of the year, and the total amount (savings + dividend) will roll over to the next year and earn dividends.

So for example, if your total savings for the year is ₱12,000 and the annual dividend is ₱461.50, then the total amount of ₱12,461.50 will roll over to the next year. You can then use this amount as the basis for your dividend computation for the succeeding year.

Final Thoughts

The Pag-IBIG MP2 savings program is a great way to save your money and make it grow at the same time. Conservative investors with a low appetite for risk may find it appealing, while ordinary Filipinos can use it to grow their money quicker instead of putting it in a low-interest bank account. And since it’s guaranteed by the Philippine government, you will get your initial investment back no matter what happens.

If you have any questions or concerns about Pag-IBIG MP2, contact the Pag-IBIG Fund by emailing [email protected] or calling the 24/7 hotline number (02) 724-4244.